What I’m Doing in This Market Correction

Meta triggered an AI drawdown. Is it justified, or a buying opportunity?

In this article, I’ll explain the current situation in the AI trade and what I’m doing.

First, we need to understand what is happening.

The Sell-Off

On Wednesday, the S&P 500 fell 0.2% and the Nasdaq dropped 0.7%.

The semiconductor index fell 6.3% on the first trading day after the sector’s best quarter on record. Micron dropped 11%, wiping out $140 billion of market value in a single session. SanDisk lost 11%, Applied Materials fell 10%, Intel dropped 9%, and AMD fell 7%.

The sell-off was heavily concentrated in semiconductors, which requires some context.

Micron, Intel, and AMD added $2 trillion of combined market value in Q2 alone. The VanEck Semiconductor ETF gained 82% in the first half, its best first-half performance since the fund launched in 2000. Micron was up 260% year to date going into Wednesday.

Bernstein had already published a cautious note on Monday comparing neocloud economics to colocation, flagging GPU depreciation, financing costs, and operating complexity as the key risks to profitability.

The AI buildout trade was priced for zero doubt, then doubt arrived.

Meta: From AI Lab to Neocloud

Meta is reportedly drawing up plans for a cloud business that would sell access to AI computing power and models under an internal initiative called Meta Compute.

Two structures are reportedly under discussion:

A Bedrock-style service, where developers access models hosted on Meta’s infrastructure, including Muse Spark, the closed-weight model Meta shipped in April.

A raw compute business, which is effectively the neocloud model.

The plans are still in development and could change. But this comes after Zuckerberg had already said in May that selling excess compute was “definitely on the table.”

The market was so stretched that what moved stocks was not an actual product launch, but a reported intention.

Meta itself closed up 9% on Wednesday. Investors liked the idea of monetizing a capex bill guided as high as $145 billion this year, instead of relying only on LLMs that appear to be going nowhere and are becoming less competitive with Anthropic and OpenAI frontier models.

The companies hit hardest were Meta’s compute suppliers.

CoreWeave fell 14% to $86, while Nebius dropped 17% to $229.

Both count Meta as an anchor customer, with a disclosed $21 billion commitment at CoreWeave and an agreement worth up to $27 billion at Nebius. A Meta that builds enough capacity to sell the excess is a Meta that may eventually rent less capacity from others, while also competing for external workloads.

Beyond the hit to its most direct suppliers, this creates a dangerous narrative:

If Meta has excess compute, maybe the AI buildout is overbuilt.

Once that narrative exists, every long AI hardware trade gets sold at the same time, especially the highest-beta names in data centers, photonics, and memory.

Macro: Not Enough

Thursday’s jobs report, released a day early because of the July 4 holiday, should have been fuel for growth assets.

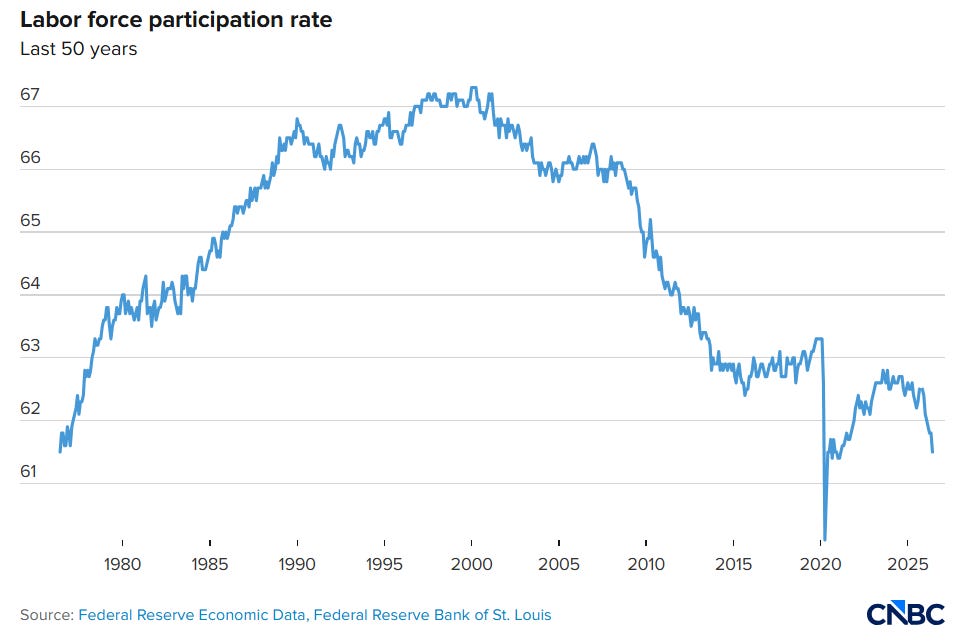

Nonfarm payrolls rose by just 57,000 in June, below expectations of 110,000 to 115,000. April and May were revised down by a combined 74,000 jobs.

The unemployment rate fell to 4.2%, but for the wrong reason: labor force participation dropped 0.3 percentage points to 61.5%, the lowest level since March 2021, while household employment fell by 507,000.

Leisure and hospitality shed 61,000 jobs, its worst month since 2020.

This was a very soft report.

Consequently, September hike odds fell from the mid-60% range to a coin flip, with the remaining hike bets pushed toward Q4. The two-year yield slipped to 4.12%, the dollar index fell about 0.5%, its biggest one-day drop in two months, and gold moved above $4,100.

With Warsh’s Fed holding rates at 3.50% to 3.75% behind a hawkish June dot plot, the weak print should have been a pressure relief valve for long-duration assets.

Not for the AI trade, though.

The Dow added 595 points, rising 1.1% to a record close of 52,900. The S&P 500 finished flat, even though most of its members advanced.

In contrast, the Nasdaq fell 1%, and the semiconductor ETF dropped another 5%. Teradyne fell 14%, KLA dropped 12%, and Micron lost another 6%. Even Meta gave back 4%.

Across the two sessions, SOXX lost 13%, its sharpest two-day drawdown since March 2025.

Memory: The Most Leveraged Bet

For better or worse, memory is treated by the market as the most cyclical part of the AI trade.

So when the market hears “overcapacity,” memory gets sold first and questions are asked later.

Korea is where that reflex did the most damage.

The KOSPI closed down 8% at 7,648, falling back below 8,000 only weeks after crossing 9,000 for the first time.

SK Hynix fell 15% to ₩2,187,000, while Samsung Electronics dropped 9% to ₩286,000. SK Square, Hynix’s largest shareholder, lost 13%. Samsung Electro-Mechanics fell 13%, and the KOSDAQ dropped 7%.

The open was violent enough, down 5.4%, that the exchange halted trading for five minutes.

This was the third Korean trading halt in under three weeks, all triggered by the same two stocks, which now represent half of the KOSPI’s weight, compared with about a quarter at the end of last year.

The difference in sentiment by investor class was clear:

Foreign investors net sold ₩5.2 trillion of KOSPI stock on the day.

Domestic retail investors absorbed ₩5.4 trillion.

The drawdown spread through the Asian supply chain. SMIC fell 11% and Hua Hong dropped 14% in Hong Kong, while Kioxia fell 10% in Tokyo after a 600% year-to-date run.

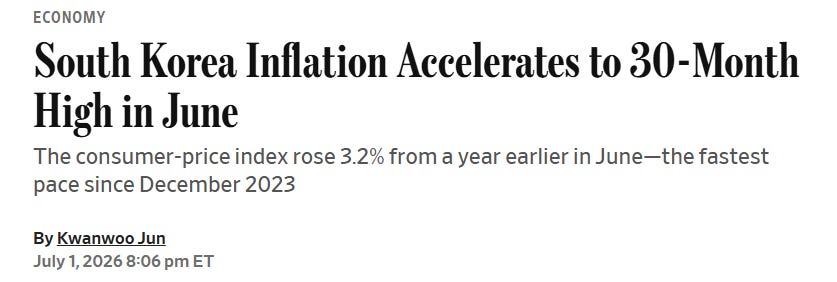

Korea’s own macro backdrop did not help either. June CPI printed 3.2%, the highest level since December 2023, strengthening the case for a Bank of Korea hike ahead of the next monetary policy meeting on July 16.

The Other Side of the Coin

On the same day, SK Hynix CEO Kwak Noh-jung detailed a ₩100 trillion, or $64 billion, domestic investment plan:

₩80 trillion for the M17 NAND fab, with construction starting next year and operations targeted for H1 2029.

₩20 trillion for the P&T7 advanced packaging facility.

This sits inside the previously announced ₩1.1 quadrillion expansion program, and comes just days after Seoul unveiled a combined ₩800 trillion national semiconductor plan with Samsung.

Does a semiconductor sell-off make sense given the acceleration in fab capacity expansion?

At the micro level, probably not.

But at the macro level, maybe. These capex plans become more fragile if hyperscaler AI capex starts to slow.

Management teams are telling investors they see enormous multi-year demand for HBM, DRAM, and enterprise NAND.

The market is interpreting something else:

Meta excess compute + rapid future supply growth = lower prices.

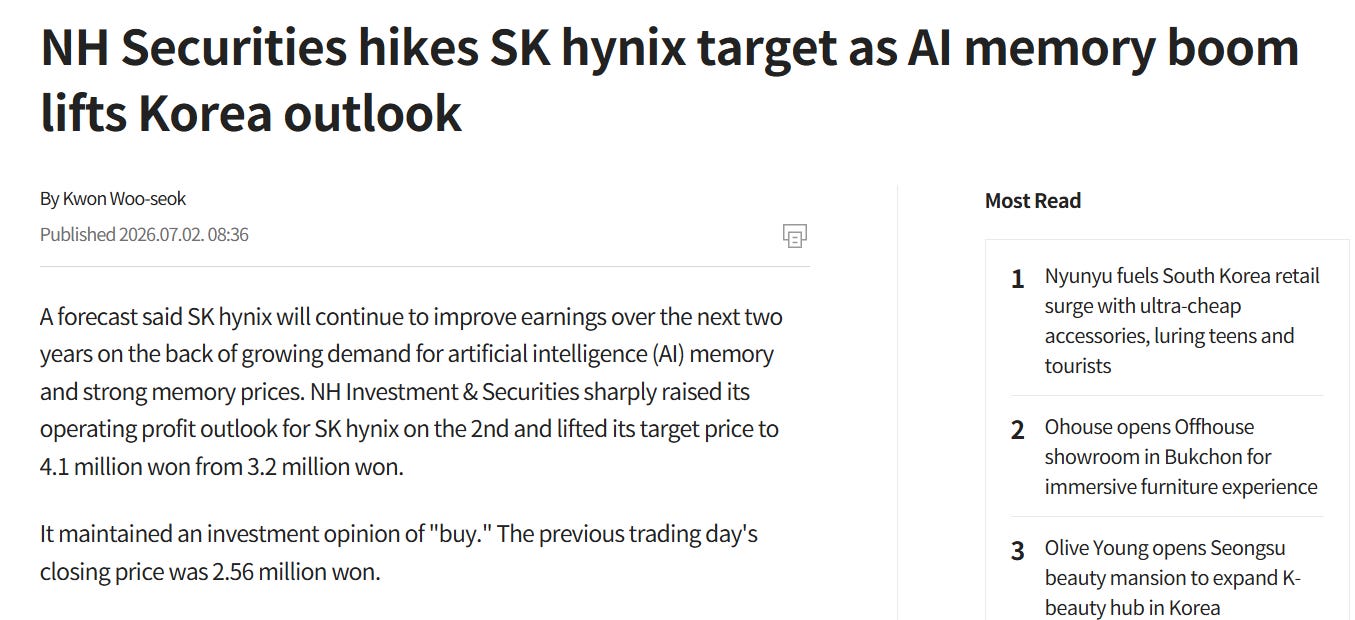

In sharp contrast with live sentiment, IBK and NH raised their Hynix targets to ₩4.0 million and ₩4.1 million on the same day the stock fell 15%. Morningstar had also lifted fair values on both Korean names on Wednesday, calling the memory cycle “tracking substantially stronger than expected,” while warning that the capacity now being added could set up a correction later in the decade.

In Micron’s case, the median analyst target sits near $1,550, with Cantor and Barclays both at $2,000.

There is also a secondary, less relevant headwind.

A class action was filed on June 25 in California federal court alleging that Samsung, SK Hynix, and Micron coordinated to restrict DRAM supply, citing 700% price increases over four years.

I wouldn’t worry about this, but it’s not ideal for an already noisy industry.

In summary, memory stocks are being treated as an instrument that the market holds when times are good and sells without hesitation at the slightest sign of problems in the AI buildout.

The “Excess Compute” Fear

Meta selling compute can mean several very different things. It does not automatically mean there is a market-wide structural flood of compute.

It could mean:

Meta overbought or misallocated capacity.

Meta wants to monetize idle capacity between internal training and inference cycles, which hyperscalers already do routinely.

Meta’s model and product execution is lagging its infrastructure spend, which is bearish for Meta’s AI ROI, but not automatically bearish for the supply chain.

Meta is turning infrastructure into a commercial cloud product, which arguably validates that compute is valuable enough to sell.

It would be one thing if Meta were selling compute at liquidation prices, but that is probably not what is happening.

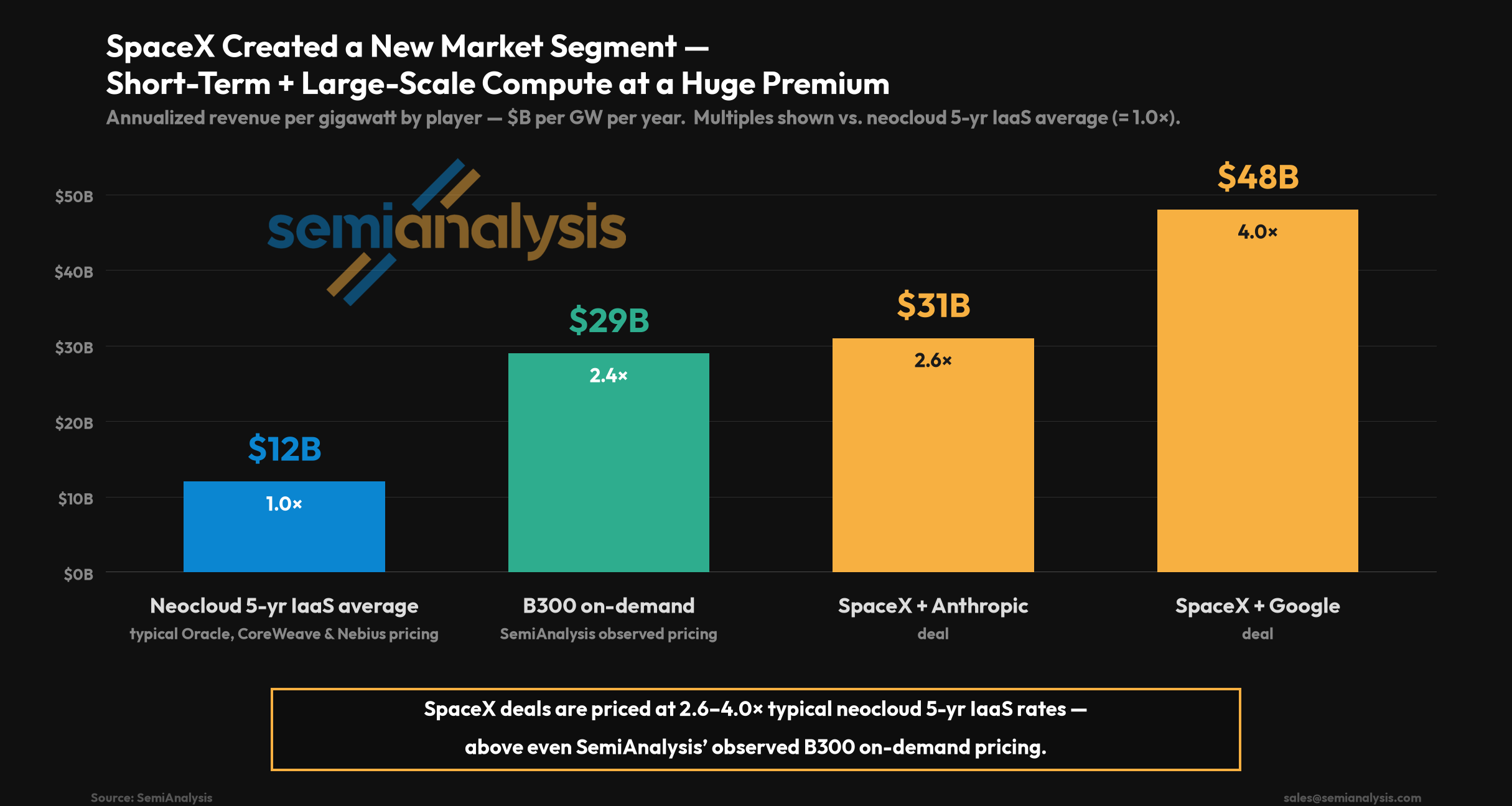

SpaceX/Google Deal

Meta is likely trying to capture rates similar to the deal SpaceX signed with Google, which were very generous. If anything, that signals compute is still scarce and valuable, just not necessarily valuable for underperforming AI labs.

SpaceX secured pricing that was 4x the five-year neocloud average, which makes it easy to understand why Zuckerberg would want to pursue a similarly profitable opportunity.

In fact, just four days before this drawdown, we got highly contradictory rumors suggesting that Google had been rationing Meta’s access to Gemini since March because Meta wanted more capacity than Google could supply.

According to those rumors, Meta was forced to tell staff to conserve tokens, while other Google customers were also affected, though to a lesser degree.

Moreover, Pichai has called Google “compute-constrained in the near term.” Google Cloud’s backlog has doubled to more than $460 billion, capex is running above $180 billion this year, and Google is still reportedly renting bridge capacity from SpaceX at around $920 million per month for 110,000 GPUs.

This is another sign that Meta may have excess compute, but the industry does not, and what matters is the latter.

These numbers do not point to excess compute. Compute is extremely valuable for companies that know how to extract value from it.

What we are seeing is the free market allocating compute toward the players that can monetize it most efficiently.

Meta: Still an AI Lab

Moreover, Meta does not seem to have thrown in the towel on frontier models entirely.

In a recent post from Alexander Wang, Meta’s head of AI confirmed that the company is training an Opus-level model for coding.

This suggests that Meta may enter the neocloud business as another way to profit from AI, while its capex remains strong and its commitment to training frontier models stays alive.

Neoclouds: An Unclear Threat

The risk for neoclouds comes down to basic supply and demand dynamics.

If AI labs like xAI and Meta go from being huge compute demanders to huge compute suppliers, that could shift the supply/demand equilibrium.

It would be similar to AMD or Amazon becoming memory resellers instead of simply using memory themselves. Sure, NVIDIA and Broadcom would still demand memory, but if you are a memory supplier, you want a market with the highest number of potential buyers and the lowest number of potential sellers.

The same logic applies here.

If Meta sells raw capacity, it could become less dependent on CoreWeave and Nebius. And if hyperscalers broadly start reselling unused capacity, GPU-hour pricing could compress unless demand from other AI labs grows even faster on a relative basis.

However, in the case of Nebius, for example, most capacity is already tied to highly profitable contracts. Combined with the blueprint of the SpaceX/Google deal and the rest of the compute shortage across the industry, a high-quality neocloud like Nebius is not highly exposed to spot pricing.

More importantly, there is no reason to assume GPUs will suddenly be sold at liquidation prices just because of this move by Meta.

If Zuckerberg decided to pursue a neocloud strategy, it would be absurd to assume it is because he sees a compute flood coming and GPUs being sold for pennies. He clearly sees a shortage, just not inside Meta, and plans to take advantage of it by supplying the successful AI labs creating that shortage.

I do not understand why anyone would think Zuckerberg would enter the neocloud business if he believed it was low-margin or that Meta’s entrance would crash prices.

I also fail to understand why the market took the SpaceX/Google deal so positively, while punishing the AI supply chain so aggressively for Meta potentially doing something very similar.

After a record year in returns, the market preferred to lock in gains before properly questioning whether the AI trade is truly under threat.

That shows how immature this industry still is from a public-market perspective.

What Would Prove the Market Right?

The market would be right to punish the AI supply chain if:

Hyperscalers cut 2027 capex.

GPU-hour pricing starts falling across contracted deals.

Neocloud utilization weakens.

Meta sells capacity at distressed pricing.

Memory pricing rolls over before new HBM and DRAM supply is absorbed.

For memory, the key risk is a 2028 supply wave arriving before AI demand is large enough to absorb it.

For neoclouds, the key risk is that contracted revenue proves less profitable after accounting for financing, depreciation, and data-center lease costs, and that steady profitability is largely never achieved.

For power developers, the risk is that they own attractive sites but fail to convert them into high-quality, financed hyperscaler contracts.

So far, nothing even close to this has happened.

In fact, everything points in the opposite direction.

However, it is still worth knowing what should make investors’ warning bells start ringing.

What Fixes This Market Pessimism?

The AI trade needs to mature from a narrative trade into a financial trade.

Right now, the market is still treating large parts of the AI supply chain as unstable and cyclical. Demand is enormous, but the path from demand to revenue, earnings, and free cash flow is still uneven.

That is what creates the violent swings.

So far, the AI trade has often been about finding the next bottleneck supplier, whether that is GPUs, HBM, power, networking, liquid cooling, data centers, packaging, or substrates.

That phase can create huge returns, but it also creates extreme narrative volatility. Stocks move violently because investors are constantly trying to price scarcity before the earnings fully arrive.

The next phase should be more mature.

It should be less about finding the next bottleneck that gets bid to stretched valuations, and more about owning the companies that can turn AI demand into revenue and earnings efficiently.

That is how mature supply chains work:

Demand becomes revenue.

Revenue becomes margins.

Margins become cash flow.

Cash flow supports higher valuations.

Neoclouds Need to Mature

Neoclouds need to prove they can become durable infrastructure businesses, not just high-beta AI capex vehicles.

The best outcome would be for the strongest neoclouds to earn a status closer to AWS, Azure, and Google Cloud.

They do not need to become as large or dominant, but they do need to become businesses the market can underwrite with the same level of financial confidence.

Until then, the market will keep treating them as risky AI infrastructure intermediaries with heavy fixed costs and uncertain long-term pricing power.

Memory Needs to Prove This Cycle Is Different

The market still assumes high memory prices eventually create too much supply, followed by a crash.

For the pessimism to fade, memory prices need to remain resilient through the next few years, even as new supply comes online.

The key proof will be that AI has structurally changed the demand curve.

That is when Samsung, SK Hynix, and Micron can rerate more meaningfully, not just through aggressive upside swings, but through consistently double-digit forward earnings multiples.

AI Needs Productivity Proof

The biggest proof is productivity.

AI will not feel like a safe long-term investment until the productivity gains clearly justify the multi-trillion-dollar capex cycle.

Companies around the world are spending enormous amounts on AI, which now needs to move from impressive demos to measurable business impact.

Once investors see that AI capex produces real productivity gains, the market will stop asking whether the spending is a bubble and start asking which companies capture the most value from it and which companies support it.

My Take and What I’m Buying

Keep reading with a 7-day free trial

Subscribe to Daniel Romero to keep reading this post and get 7 days of free access to the full post archives.