What I’m Buying in This Dip

When the market dips, the best option is to look for opportunities

The market is showing a lot of resilience given everything that has been going on in the world.

From Liberation Day, to the October 10 crypto crash, to the war in Iran, the world is not offering an easy environment for investors, particularly those with higher exposure to high-growth industries.

Think about it. The AI rally is based on hundreds of billions of capex. If interest rate expectations change because of inflation pressure, making the cost of debt more expensive, each additional percentage point can translate into billions in extra cost.

Unfortunately, it seems like it may get worse before it gets better.

An Energy Crisis

The seven Persian Gulf countries produce about 32% of the world’s crude oil, hold about 49% of global proved oil reserves, and Saudi Arabia alone is estimated to hold around 17% of total proved global oil reserves.

Here is where the worrying news kicks in. France’s finance minister has said that 30% to 40% of the Gulf countries’ refining capacity has been damaged or destroyed.

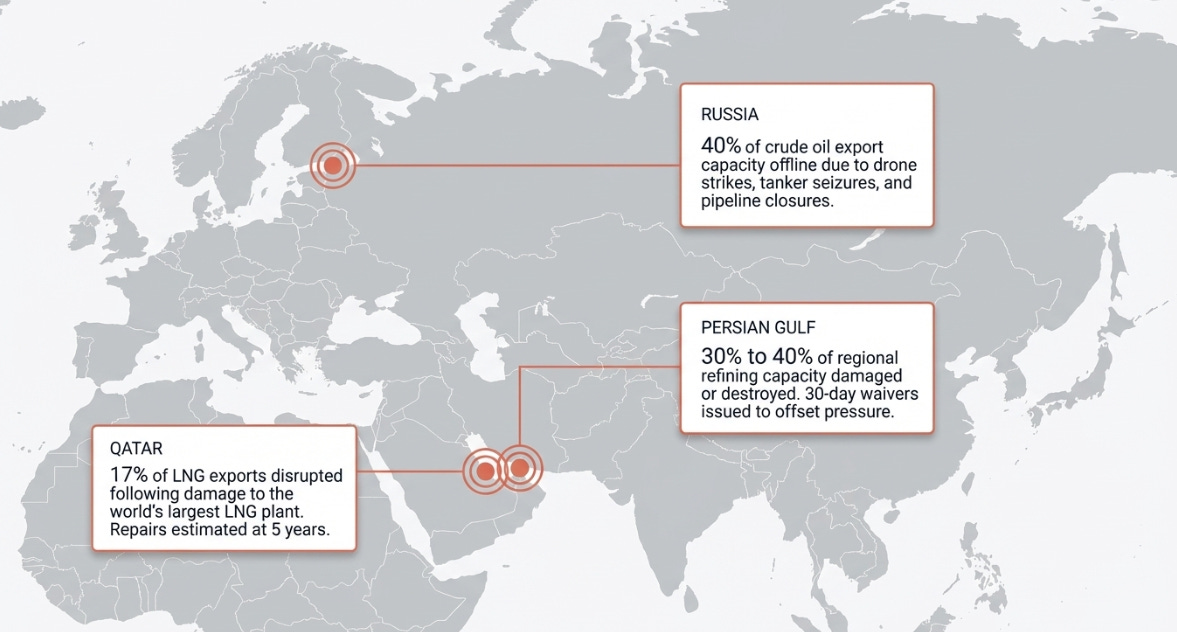

A clear example is Qatar’s Ras Laffan, the world’s largest LNG plant. Drone strikes damaged two production trains, representing about 17% of Qatar’s Las exports. According to QatarEnergy, repairs will take up to five years, affecting supplies to Europe and Asia.

Because of this pressure on oil and gas prices, the U.S. issued a 30-day waiver allowing countries to buy sanctioned Russian oil.

In response, and to prevent Russia from taking advantage of the situation, Ukraine has been targeting Russian oil infrastructure. Russia’s Baltic Sea ports of Primorsk and Ust-Luga suspended crude and oil product loadings after Ukrainian drone attacks, and Russia’s Kirishi refinery, one of the country’s largest, halted processing after fires caused by those strikes. Around 40% of Russia’s crude oil export capacity is now offline due to a mix of drone attacks, tanker seizures, and the closure of the Druzhba pipeline through Ukraine.

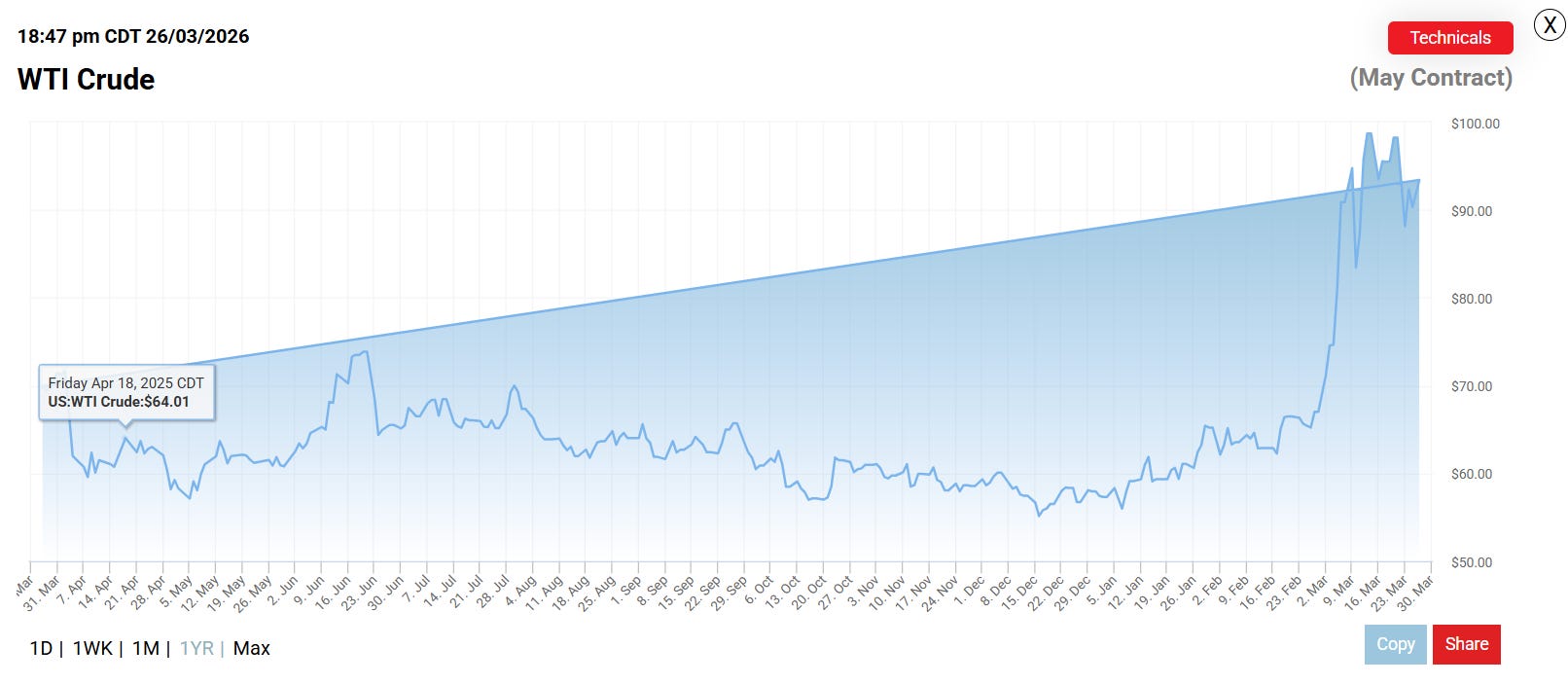

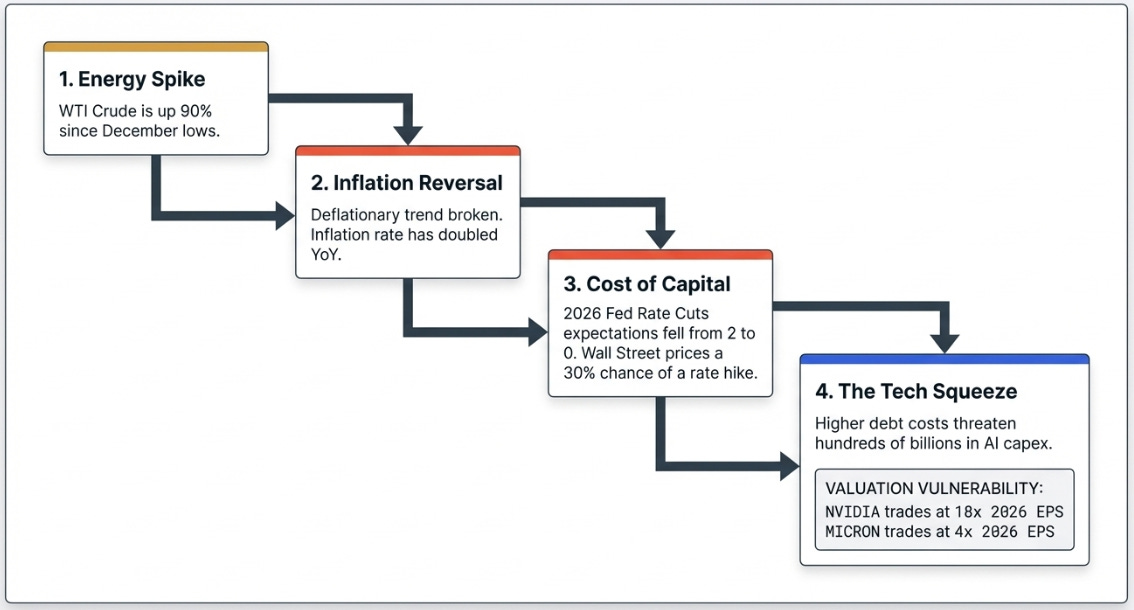

This is already having a major impact on crude oil prices, with WTI up 90% since the December lows.

Inflation and Interest Rates

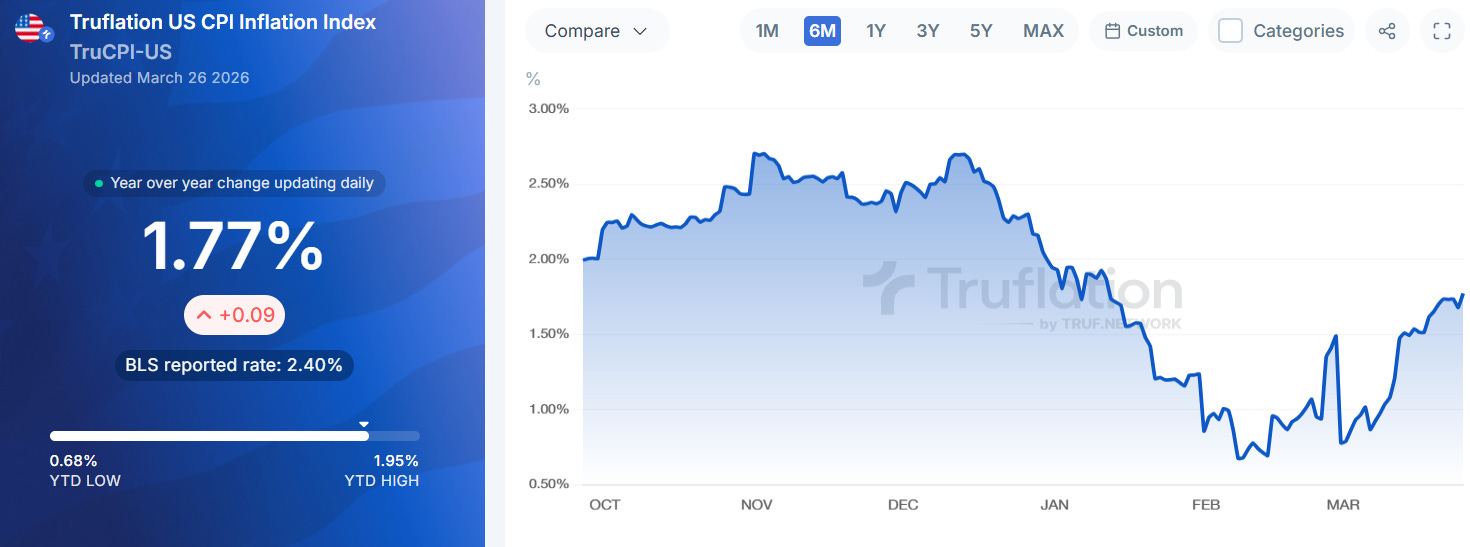

This has not taken long to be reflected in inflation. While it had been on a clear downtrend since December of last year, the current situation has shifted that trend, and now the inflation rate has more than doubled on a YoY basis.

As of January 1, 2026, the clear answer is that the market was pricing in about two Fed cuts for 2026.

Unfortunately, that expectation has now fallen to zero cuts, which explains much of the market movement we are seeing.

In fact, Wall Street now sees a 30% chance of a rate hike.

How fast expectations can change.

This is why NVIDIA is trading at 18x 2026 earnings and Micron at 4x. If capital market conditions worsen, there may be cuts to AI spending over the coming months, or even years, which would put a stop sign in front of these companies’ growth.

The situation is so severe that the International Energy Agency called it the largest disruption to global oil markets in history. However, it is not catastrophic. The IEA still expects global oil supply to exceed demand by 2.46 million bpd in 2026, even after lowering its previous surplus estimate, and noted that Saudi Arabia and the UAE are expanding export routes that bypass Hormuz. The UAE and Saudi Arabia also have about 2.6 mb/d of unused capacity through existing pipelines that could help bypass Hormuz. That is not enough to replace the Strait, because more than 20 million barrels per day normally pass through it, but it is enough to avoid a complete halt in Gulf exports.

There is also the safety net of inventories and emergency reserves. The IEA said global observed oil inventories were above 8.2 billion barrels in January 2026, the highest level since February 2021, and member countries agreed on March 11 to release a record 400 million barrels from emergency reserves.

Geographical Impacts

Not all countries are equally affected.

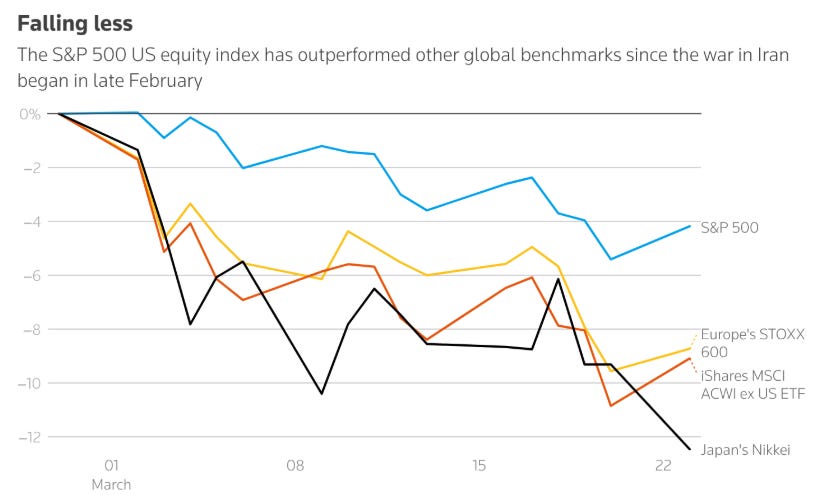

The S&P 500 has fallen about 4% since the war began, versus about 9% for Europe’s STOXX 600 and more than 12% for Japan’s Nikkei.

One stat that helps explain this is that the shift toward a more services-based economy, away from manufacturing, along with access to more diverse energy sources, has made the U.S. economy less dependent on oil, whose price has surged more than 30% since the crisis began. Compared with 1980, it now takes 70% less oil to produce the same amount of GDP, according to a report by Morgan Stanley.

Another reason is that only 4% to 8% of U.S. oil comes through Hormuz, and the United States is a net exporter of petroleum and gas.

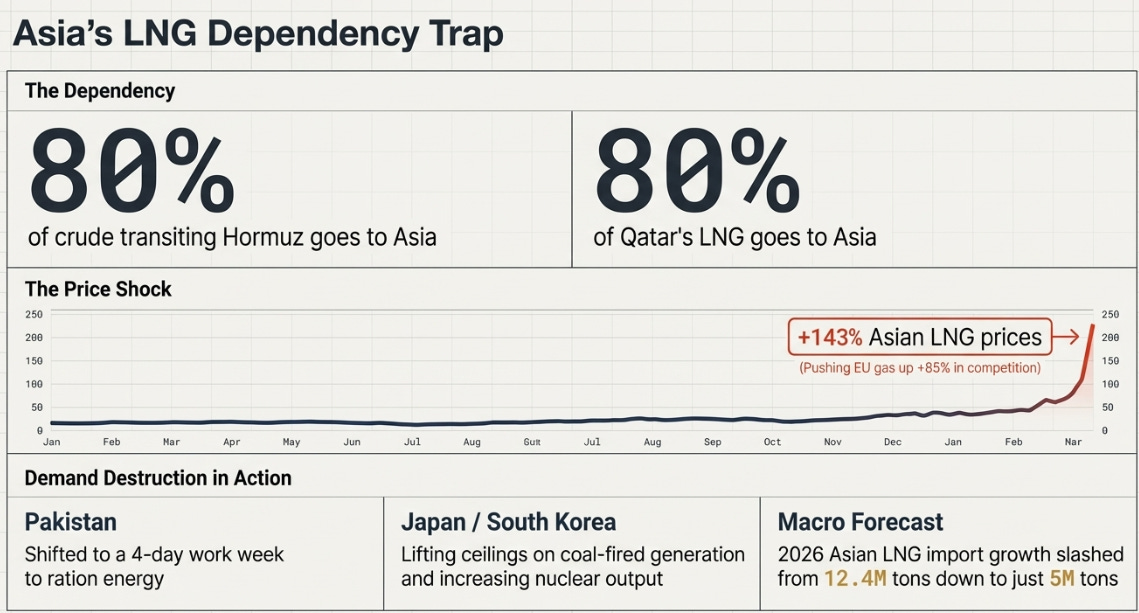

In contrast, Asia buys more than 80% of the crude that transits the Strait of Hormuz, and 80% of Qatar’s LNG goes to Asia. Asian LNG prices have jumped 143% since the war began on February 28. The EU’s main gas suppliers are Norway and the United States, but it now has to compete with Asian countries for supply, which has pushed gas prices in Europe up by 85%.

In response, there is already significant demand destruction. Pakistan has moved to a four-day work week to ration energy, while Bangladesh, India, and other price-sensitive buyers are seeking replacement cargoes and shifting toward coal and domestic gas. Forecasts for Asian LNG import growth in 2026 have been reduced to about 5 million tons from 12.4 million, assuming a two-month Middle East disruption. South Korea plans to remove ceilings on coal-fired generation and increase nuclear output, while Japan’s JERA said it would keep coal plants running at high utilisation.

Fertilizer Bottleneck

Beyond energy, the biggest issue may be fertilizers. Around 30% of globally traded fertilizers normally move through Hormuz. Gulf producers are major suppliers of ammonia and urea, and urea prices were already up 30% to 40%. There are no strategic global fertilizer stockpiles, which makes the shock harder to absorb than it is for oil. Two of the most affected countries are China, which gets more than 50% of its sulphur imports from the Middle East, and Indonesia, which gets nearly 70% from the region.

The disruption has hit right as the Northern Hemisphere spring planting season began. Farmers still needing to buy fertilizer are being hit at the worst possible moment, and some may respond by using less fertilizer or shifting away from nitrogen-intensive crops such as corn. Higher prices are likely to show up first in corn and wheat, and later in feed, dairy, meat, bread, poultry, and eggs.

Fertilizer costs in Somalia, Bangladesh, Kenya, and Pakistan, some of the countries most affected, have already increased by more than 40%.

The situation is even worse because the market was already undersupplied before the war began. China had already been restricting fertilizer exports to protect domestic supply, Europe had cut output after losing cheap Russian gas, and now China has started releasing fertilizer from its reserves early to stabilise its domestic market. Russia controls 40% of global ammonium nitrate trade and has also suspended ammonium nitrate exports for a month to protect domestic supply.

Semiconductor supply chain

Taiwan

Taiwan has sufficient domestic petroleum and LNG inventories to meet demand for March and April, and the government has signed new contracts to increase U.S. natural gas imports starting in June.

In terms of helium, a key gas used in semiconductor manufacturing, Air Liquide, an important supplier to Taiwan’s semiconductor industry, said a short-term helium shortage is expected, but that it would reallocate supply from other regions to address the issue. Taiwan’s economy ministry said helium supply remained stable, with imports now available from the U.S.. GlobalWafers said it had reviewed inventories of helium and other key materials and had enough confirmed supply for multiple years, while TSMC said it does not currently expect any significant impact.

So, while manufacturing costs will increase, which could have a short to mid-term effect on the margins of companies like TSMC, the situation is not catastrophic.

South Korea

South Korea supplies about two-thirds of global memory chips, which makes it a crucial player in the semiconductor supply chain. The country also relies heavily on the Middle East for 14 chip-supply-chain items, including helium, bromine, and chip inspection equipment.

On the positive side, SK hynix said it had long secured diversified supply chains and sufficient helium inventory, and therefore saw almost no chance of being affected.

South Korea is the world’s No. 3 LNG importer, with 7.16 million metric tons imported from Qatar last year, and around 14% of its 2026 LNG imports expected to come from Qatar. Korea’s public natural gas company, KOGAS, has inventories above mandatory reserves, and the government is ready to increase coal and nuclear output while reducing gas-fired generation if needed.

In summary, just as with Taiwan, investors should expect higher manufacturing costs, gross margin compression, and, depending on how demand dynamics evolve, an even more severe memory shortage.

Japan

Japan has LNG stockpiles equal to about three weeks of consumption and oil stockpiles equal to 254 days of net imports. Qatari LNG accounts for about 4% of Japan’s total LNG imports, while the broader Middle East accounts for about 11% of Japan’s LNG and around 90% to 95% of its crude oil.

JERA, Japan’s biggest LNG buyer, said it faces no immediate LNG supply threat, but is seeking additional cargoes and added that, if the crisis deepens, Japan may need to consider energy conservation and even restart more coal-fired plants.

Petrochemical companies are cutting output, refinery runs have fallen below 70%, and one JFE Steel power facility was shut due to heavy-oil shortages.

Japan is a crucial supplier of semiconductor materials, specialty chemicals, and equipment, so while there are no reports yet of a specific material shortage, higher energy prices will inevitably affect it in a similar way to its Asian neighbors.

In summary, the war will most likely create inflationary pressure worldwide, and the longer it lasts, particularly if the Strait of Hormuz remains closed, the longer those inflationary effects will persist.

The country that is overall less affected by the situation, although still heavily exposed because we live in a globalized world, would be the United States. Its strong petroleum and gas position, combined with the fact that its citizens spend a much lower percentage of their income on food than in most Asian countries, turns a global crisis into a milder economic problem.

What opportunities could this create in the stock market?

I will not talk here about trade ideas to take advantage of the supply chain disruptions.

I already shared some ideas after the war started, and this is how they have performed over the last month:

Equinor (EQNR): +43%

Major gas supplier to Europe.Linde (LIN): -1%

Industrial gases leader.NewMarket (NEU): 0%

Specialty lubricant and fuel additives.Woodside Energy Group (WDS): +16%

Australia-based LNG and upstream producer.Santos (STO:ASX): +18%

Australian gas and LNG producer with Asia-linked demand.Kinder Morgan (KMI): +3%

U.S. natural gas pipelines and storage.Cheniere Energy (LNG): +24%

Core U.S. LNG exporter.ConocoPhillips (COP): +20%

Large-scale upstream crude producer with diversified barrels.

I am going to talk about five positions I am buying more aggressively.

Let’s start.

Keep reading with a 7-day free trial

Subscribe to Daniel Romero to keep reading this post and get 7 days of free access to the full post archives.