Tempus AI: Deep Dive

Tempus AI is positioning itself as the AI backbone of healthcare, targeting a multi-trillion-dollar opportunity

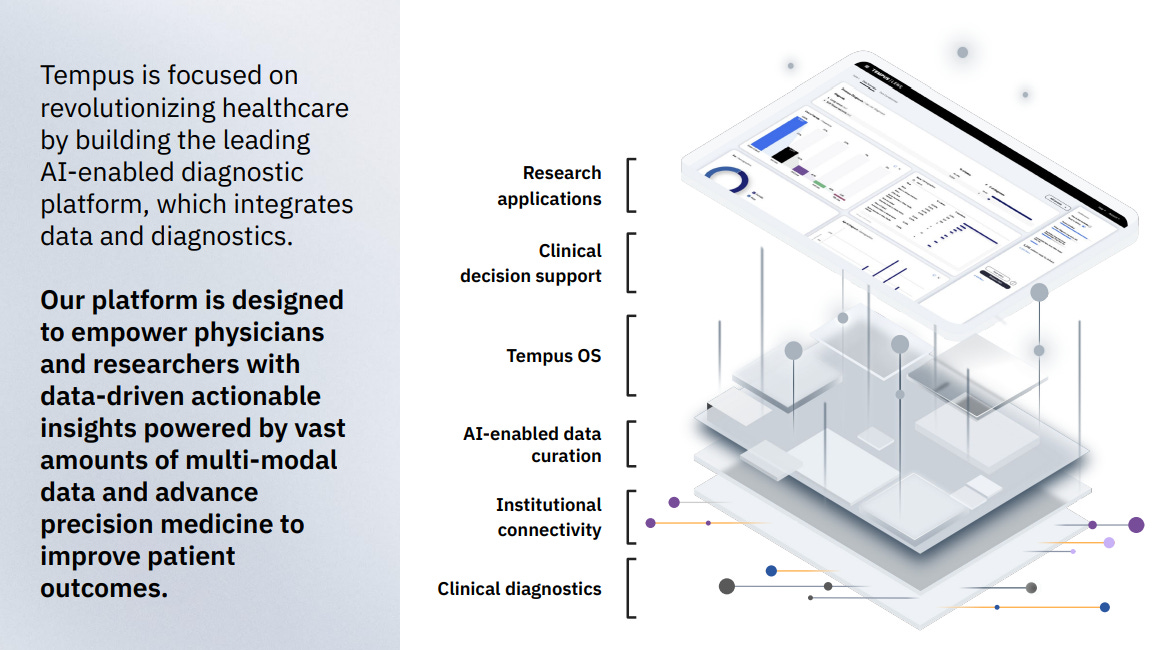

Tempus is an AI-driven precision medicine platform that is rapidly becoming core infrastructure for modern United States healthcare. It is already deeply integrated into clinical workflows, widely used by leading pharmaceutical companies, and building a growing data advantage that few businesses can realistically replicate.

Yet it is still underfollowed.

It trades at around 6x next-twelve-month sales, has FDA-approved AI diagnostics, is used by 95% of top pharmaceutical companies, and owns the type of data moat that becomes more valuable over time. There is a strong case that Tempus is quietly becoming the AI backbone of American healthcare.

Let’s dig in.

Disrupting Healthcare From Within

Tempus is not just a software company with a large data repository. It goes much further. The company is already embedded across the healthcare system, which gives it access to real-time data that continuously improves its AI models.

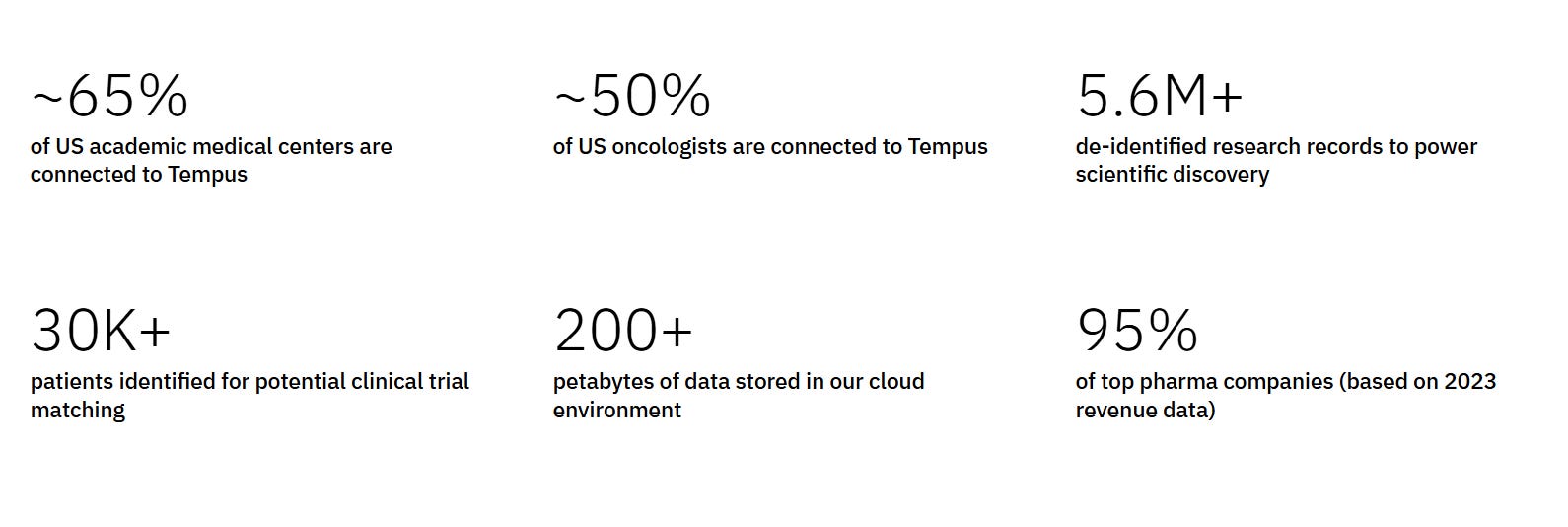

Its tools are used by 95% of top pharmaceutical companies, including AstraZeneca, Recursion, and Pfizer. With a strong oncology focus, Tempus is connected to more than 65% of academic medical centers and over 50% of United States oncologists through its sequencing and data-collection network.

That creates a defensible moat that is very difficult to replicate.

You cannot simply fund a startup and expect to compete with Tempus. Healthcare data is highly sensitive, heavily regulated, and difficult to aggregate at scale. Tempus has already secured a position inside a uniquely valuable data ecosystem.

Its access includes not only real-time patient data, but also extensive clinical records, imaging information, and biological data generated from the patients it serves. This creates a significant and expanding advantage in the race to build the most capable healthcare AI.

All of this data is interconnected through Tempus software, which uses AI to identify patterns across millions of patients. The combination of large-scale datasets and advanced AI is extremely powerful.

Leading AI researchers often highlight that the main bottleneck is not the algorithms, it is data quality. In healthcare, high-quality data is scarce, private, and difficult to access.

Tempus not only has access to some of the best data in the industry, it is also applying that data in real time to improve model performance. This strengthens its position as a potential long-term AI leader in healthcare, with a deep moat built on a unique data advantage.

Tempus is also backed by notable investors, which adds credibility to the company and supports confidence in the long-term story.

Google with approximately 1% ownership

Novo Nordisk with approximately 2.5% ownership

A Diversified Business Model

The business is built around three primary revenue streams:

1. Genomics (diagnostic testing)

This is the foundation of the business. Tempus provides DNA and RNA sequencing, molecular profiling, and germline testing across a wide range of conditions, with a strong focus on oncology.

The company runs high-quality tests that combine tumor data with clinical context, giving physicians actionable insights rather than isolated mutation lists. These tests are typically paid through insurance reimbursement or direct payment from providers and research partners.

Volume: millions of tests processed to date

Use cases: personalized treatment decisions, clinical trial matching, and disease monitoring

Key differentiator: integration of structured clinical history, genomics, and imaging into one diagnostic report

In a conventional diagnostic workflow, value often stops at the result. In a Tempus workflow, the result is the starting point. The added value comes from context.

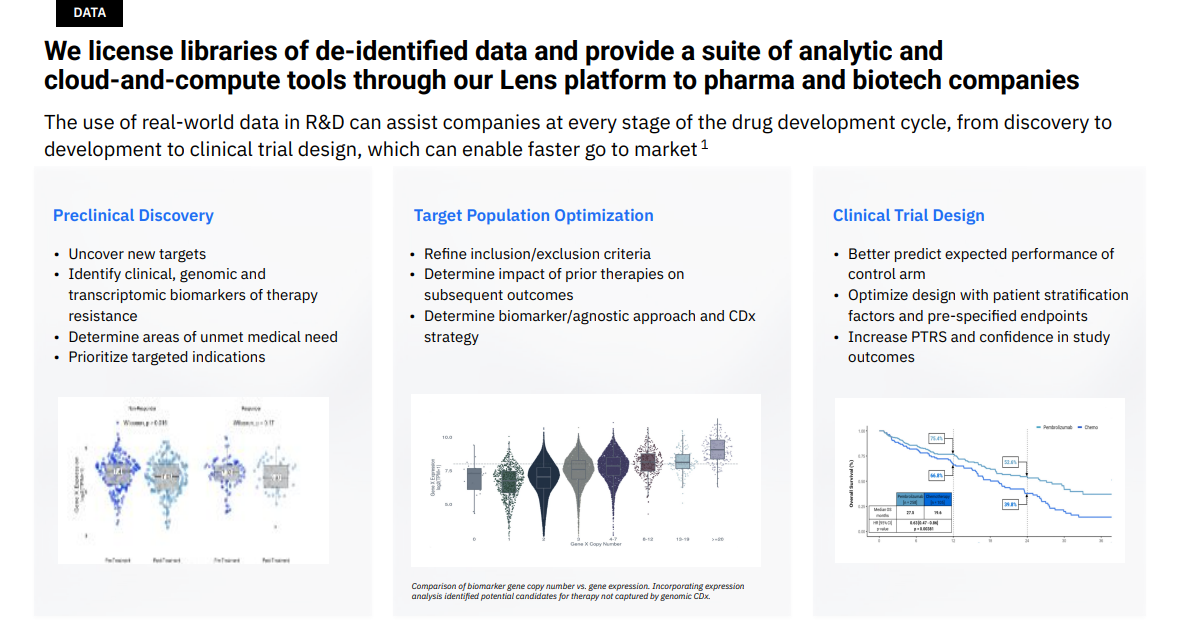

2. Data Licensing and Services

Sequencing and clinical testing generate structured, de-identified data, exactly what pharmaceutical companies need for drug development, clinical trial design, and AI model training.

Tempus licenses this data to 19 of the top 20 pharmaceutical companies, which use it to identify patient populations, improve molecule selection, and model clinical pathways.

Dataset: more than 8.5 million fully structured cancer patient records, plus over 11 million partially structured records

Scope: genomics, clinical data, imaging, digital pathology, and patient outcomes

Platform tools: Lens, Hub, Pixel, and Link for querying, analysis, and visualization

This is one of the highest-margin parts of the business, with gross margins between 75% and 80%. Tempus also has more than 900 million dollars in signed contracts, with most of that expected to convert into revenue over the next several years.

3. AI Applications

This is still a small share of revenue, but it may be the most transformative over the long term. It includes AI diagnostics, clinical decision support tools, and trial-matching algorithms, many of which are already FDA-approved and used in active clinical settings.

In 2024, this segment generated about 7.5 million dollars, representing roughly 1.5% of revenue. That could change materially if AI-based tools receive broader reimbursement and adoption scales.

Tempus has already built an integrated AI platform that includes:

ONE: patient data navigation for clinicians

Next: AI-assisted clinical trial matching

Lens: analytics and cohort selection

Pixel: imaging and radiomics interpretation

Link: provider coordination platform

Hub: central data and algorithmic dashboard

Each product is built to integrate directly into real hospital workflows. The objective is clear: clinicians should be able to access up-to-date patient data instantly and use AI support to make better decisions faster.

With Tempus, clinicians can receive real-time analysis, summaries of patient history, drafted letters, structured interpretations of lab and imaging results, and treatment guidance based on patient-specific data. The platform is designed to improve decision quality while reducing time burden.

Consider the pace of change in medicine: new research, new therapies, new diagnostics, emerging diseases, and continuously evolving drug pipelines. The information load is massive, and Tempus helps healthcare professionals manage that complexity more effectively.

By combining broad medical data access with an intuitive, efficient, AI-powered platform, Tempus helps clinicians work more effectively and improve patient outcomes.

There is nothing more convincing than hearing a practicing physician explain how Tempus has made them more productive and more effective in clinical care:

Strategic Acquisitions

Tempus is expanding its ecosystem through high-value strategic acquisitions.

Ambry Genetics

Acquired for 600 million dollars (375 million dollars in cash and 225 million dollars in stock), Ambry is one of the most established and trusted genetic testing companies in the United States, processing more than 400,000 patients per year.

This transaction adds several strategic benefits:

Immediate scale in hereditary and germline testing

Expanded exposure to cardiology, rare disease, pediatrics, immunology, and reproductive health

West Coast lab infrastructure

Access to additional partnerships, clients, and datasets

Ambry is highly complementary to Tempus’ oncology foundation and strengthens its ability to deliver full-stack, population-scale genomic screening.

Deep 6 AI

Another major move was Deep 6. The company specializes in AI-powered clinical trial matching, using natural language processing to interpret both structured and unstructured electronic health records. The platform is already connected to more than 750 provider sites, with access to data from over 30 million patients.

This acquisition adds key advantages:

Faster trial recruitment

Better patient stratification

Expanded clinical trial revenue opportunities

Improved data sourcing across diverse populations

Together, Ambry and Deep 6 strengthen Tempus’ data flywheel and support a faster path to profitability.

Collaborations

Tempus also holds a 19.3% stake in Personalis, a leader in tumor-informed minimal residual disease testing. This partnership focuses on tracking patient response to immunotherapy in lung and breast cancer through the NeXT Personal test.

The companies expect to test tens of thousands of patients over the next three years, pushing Tempus further into the growing minimal residual disease and longitudinal oncology monitoring markets.

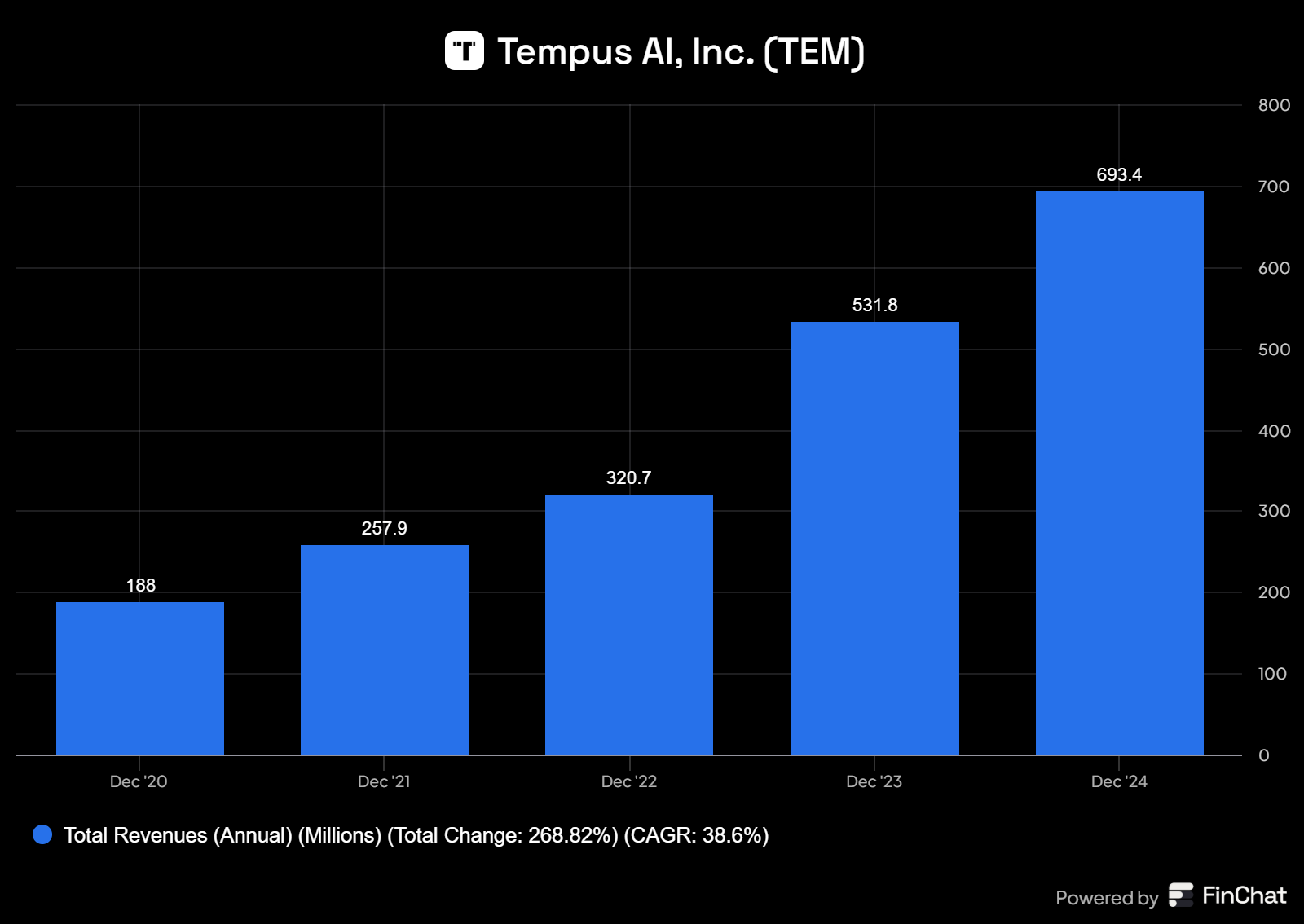

Financials

2024 revenue: around 1 billion dollars including Tempus and Ambry

Revenue CAGR over the last four years: 39%, excluding Ambry, which should further support 2025 results

2025 guidance: around 1.23 billion dollars in revenue, implying more than 75% year-over-year growth

2024 organic growth excluding Ambry: 30%

Adjusted EBITDA and free cash flow: both expected to turn positive this year

Margin profile is improving quickly:

Genomics: 45% to 50% gross margin

Data and Services: 75% to 80% gross margin

AI Applications: small today, but potentially above 90% margin at scale

Tempus ended 2024 with 340 million dollars in cash, enough to cover debt obligations. The Ambry acquisition added cost, but it also added scale and potential margin expansion.

Customer retention is strong. Net revenue retention increased from 125% in 2023 to 140% in 2024. Once partners adopt the platform, they tend to expand usage over time.

Valuation

At around 6x sales, Tempus may not look cheap at first glance. But given its:

Leadership in multimodal healthcare data

Strong network effects

Clear path to profitability

Expansion into software and AI tools

it is not difficult to see a path toward a multi-dozen-billion-dollar company over time.

If Tempus reaches 20% free cash flow margins at scale and continues to grow revenue at 25% to 30% annually, today’s market capitalization could look small in hindsight.

This is not just a cheap-stock argument. It is a thesis around a scalable, sticky, and strategically important platform in a multi-trillion-dollar industry.

Let us run a simple model.

Assume Tempus grows at a 20% CAGR for 10 years after 2025 and reaches a 20% free cash flow margin. Under that scenario, free cash flow in 2035 would be around 1.5 billion dollars.

By then, the business could still be growing. Each year it accumulates more data, develops more algorithms, and trains models on larger datasets. The moat can deepen over time. It is reasonable to expect continued expansion of AI capabilities across additional healthcare specialties, reinforcing its role as an embedded software and AI infrastructure layer.

Using a conservative 20x free cash flow multiple, the company could be worth around 30 billion dollars, versus roughly 7.5 billion dollars today. That implies about a 14.9% annualized return over a decade.

For some investors, that may not sound extraordinary. But this would still outperform long-term equity benchmarks under relatively conservative assumptions.

A company with this level of technology, data scale, and strategic relevance in a multi-trillion-dollar market could plausibly achieve higher margins. And a 20x multiple is modest relative to many software peers.

For context:

Palantir trades around 135x next-twelve-month free cash flow

Microsoft around 38x

CrowdStrike around 80x

MongoDB around 91x

If sentiment shifts, or if Tempus gains broader recognition as core AI infrastructure in healthcare, upside could be materially higher.

Final Thoughts

Tempus is not just riding the AI wave. It is building core infrastructure for AI-powered healthcare. If AI becomes central to how we diagnose, treat, and monitor disease, and I believe it will, then Tempus could become one of the most important companies in the sector.

At today’s price, Tempus may not look obviously cheap, but the long-term picture is more compelling. When you own great companies, upside surprises are common. With weaker businesses, the opposite is usually true.

Would I buy a fairly valued company that could evolve into a technology leader in the largest sector of the United States economy? I would.

If you are building a long-term portfolio to capture the AI wave through a high-quality business with a meaningful moat and real upside, Tempus deserves a place on your radar.

Is Tempus AI a good company? It has excellent long-term growth potential.