Is Nebius Overvalued?

After the Microsoft Deal: Is Nebius Still Undervalued or Time to Sell?

Introduction

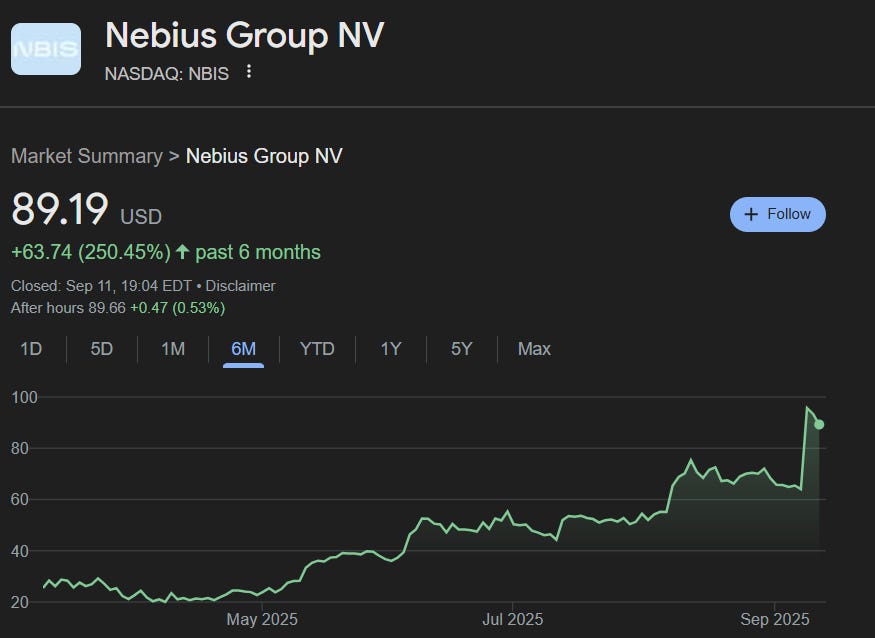

Nebius is up 250% in the last 6 months.

Everyone is wondering. At what point is this just too much? When does this company become overvalued?

Let’s not waste time and get into it.

The Microsoft Deal

For starters, I don’t think there has been a fundamental change in the thesis regarding Nebius. The Microsoft deal is more of a confirmation and a derisker of the business than a surprise.

If you were bullish on Nebius, you would have expected that capacity to be filled and that the revenue potential would be in line with what they’re now getting from Microsoft. That’s not the news. The real news is that, instead of selling capacity in smaller pieces, they’re selling it all to a single customer, none other than the second-largest company on Earth. This deal is a massive derisker, but it doesn’t change how I see the company fundamentally.

Does that mean I think it’s now fairly valued? That there isn’t more potential ahead?

Not at all. What it means is that the company was tremendously undervalued, to the point where I couldn’t believe my eyes every time I saw the valuation. This was a >$20B company since 2024. 2025 was simply their time to shine and prove it.

Now, what about their valuation today? The Microsoft deal, starting in Q2 2026, will bring almost $4B in annual revenue.

The Finland expansion, which is being finalized in Q1 2026, is expected to increase the site’s revenue potential to $1B per year.

Add the capacity from Kansas, which will likely be expanded to its full 40MW capacity by next year, and you’re already looking at about $5.5B in revenue.

On top of that, their smaller deployments in the UK, Israel, Paris, and Iceland could push revenue to $6B. All of these deployments are expected to be online by mid-2026.

This means Nebius could reach an ARR of nearly $6B by mid-2026.

What about their plans going forward? Nebius is now headed toward their second wave of growth, and the company has already signaled what they’ll do with the cash.

They need funds to finish their New Jersey site and deploy the necessary GPUs to deliver the capacity contracted by Microsoft.

On top of that, they are looking for another one or two greenfield sites in the US. They are also exploring land purchases, which could indicate an intention to build more wholly owned data centers, similar to the one in Finland, rather than relying on tenants.

What could this bring to the company in terms of revenue? I’ll go over that and discuss whether I think Nebius is undervalued in this article.

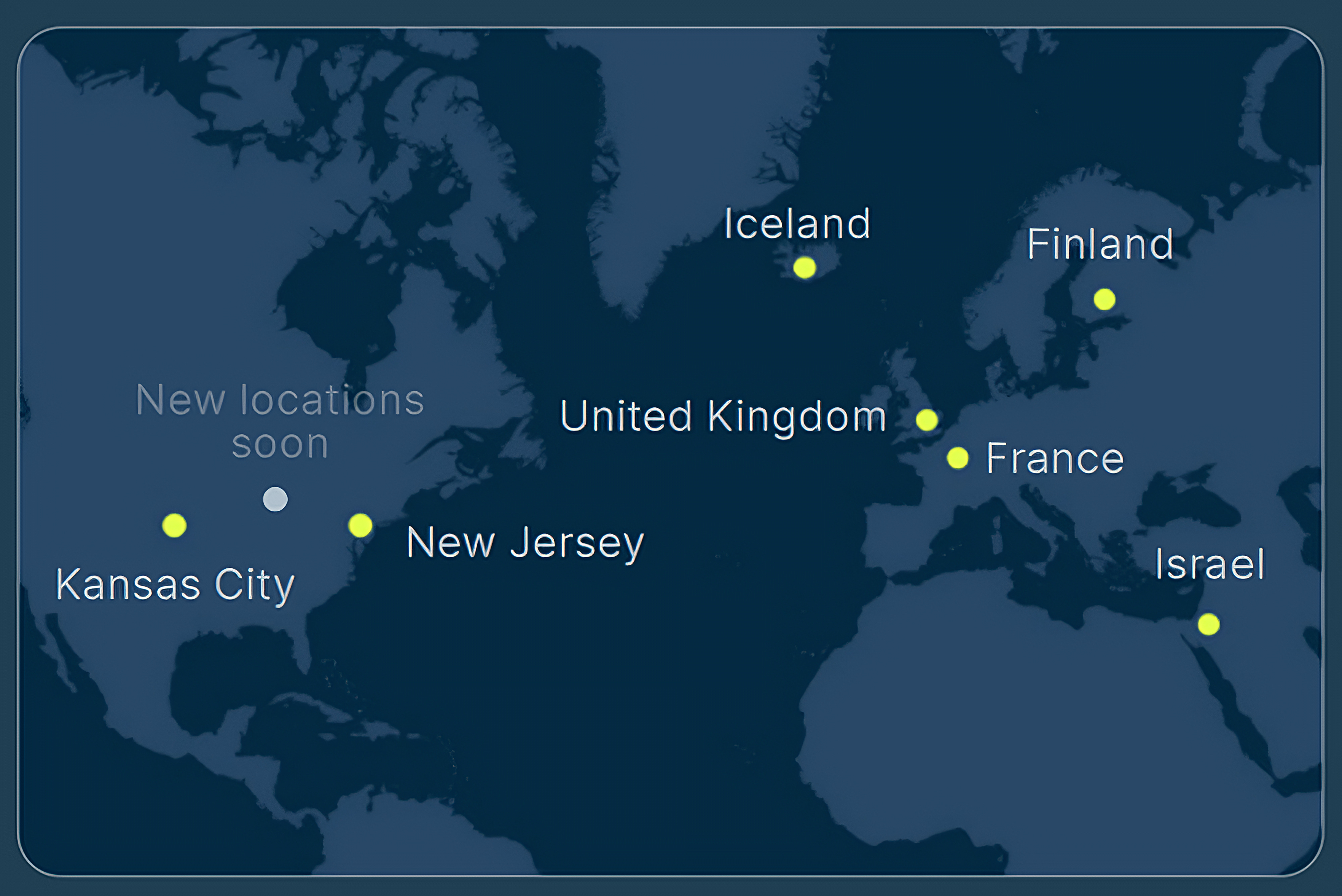

Nebius’ Footprint

Europe & Israel

Finland (Wholly Owned): Their only fully owned data center, being expanded to a 75 MW capacity. Expected to generate $1B in ARR starting next year.

France (Paris – Equinix Colocation): A smaller deployment, likely aimed at addressing local demand.

Iceland: Currently running with 10 MW of capacity.

United Kingdom & Israel:

UK goes live in Q4 2025 starting with 4,000 B300 GPUs, which will be expanded to 9,000 GPUs.

Israel is scheduled for early 2026 with 4,000 Blackwell GPUs.

United States

Kansas City: Operational since Q1 2025 with an initial 5 MW, now being expanded with Blackwell GPUs with up to 40 MW of capacity.

New Jersey: 300 MW capacity contracted by Microsoft, starting in Q4 2025 with 25 MW and gradually reaching 300 MW by Q2 2026.

Two New Greenfield Sites (Coming 2026): Nebius announced they are close to securing two massive greenfield locations in the U.S. Each is expected to deliver hundreds of megawatts of power in 2026. A formal announcement is expected soon.

Revenue Potential

With both its Finland data center and its New Jersey data center, Nebius is expected to generate between $12.5M and $13.5M per MW per year.

Considering all other capacity, and assuming they expand their Kansas data center, Nebius’ ARR will reach around $5.5B on roughly 425 MW that is live or contracted, using a midpoint of $13.0M per MW.CAPEX Funding

Does Nebius have the necessary funding? As of the end of their last quarter, Nebius held $1.68B in cash.

After the blowout deal with Microsoft, the stock rose 60% in a single day, which the company wisely took advantage of by announcing a share offering and a new convertible notes placement. This combination of debt and equity will provide an additional $4.2B in cash.

In total, Nebius now has approximately $5.9B in cash. To execute their expansion plans, the company will need to purchase large volumes of NVIDIA GPUs, which will be extremely costly.

We don’t know exactly which types of GPUs Nebius will use for all of its data centers, but there are some confirmed details.

In Finland, the original plan was to complete the site with H200s, but this shifted to GB200 systems.

In Kansas, they are also deploying HGX B200.

For the UK, Nebius is deploying 9,000 B300s.

In Israel, it will most likely be GB200s.

For New Jersey, the details are not confirmed, but I assume it will be half GB200 and half GB300 systems.

Considering these deployments, we can make a rough estimate of what it would take for Nebius to reach $5.5B in ARR.

Nebius Expansion CapEx

Finland (20 MW GB200): ~$0.5B

Kansas City (35 MW, half GB200 / half B200): ~$0.93B

Israel (4,000 GB200): $0.17B

United Kingdom (9,000 B300): ~$0.41B

New Jersey (150 MW GB200 + 150 MW GB300): ~$8.56B

Total unpaid CapEx: ~$10.6B

Cash on hand: ~$5.9B

Funding gap: ~$4.7B

So, Nebius doesn’t have enough cash to complete all projects with current balances. However, they plan to cover the gap with cash generated from operations.

After every MW of capacity Nebius brings online, Microsoft will start paying for that capacity. This means Nebius doesn’t need to finish the project with only preexisting funds. They can deliver capacity → receive payments → reinvest cash to keep expanding.

Does the math check out?

Nebius will start delivering 50 MW of capacity by Q4 2025. Those 50 MW will represent around $145M in cash flows per quarter. The plan is to finish the project by mid-2026. Assuming the following timeline:

Q4 2025: 50 MW → $145M

Q1 2026: 100 MW → $290M

Q2 2026: 200 MW → $580M

Total cash inflow: ~$1B before the entire project is finished.

Now, compare that with the CapEx requirements:

Q3 2025: $1.43B

Q4 2025: $1.43B

Q1 2026: $2.86B

Q2 2026: $2.86B

Total CapEx: ~$8.56B against ~$1B received.

This means the pre-revenue cash requirement is about $7.56B.

New Jersey is the most substantial one, but the same applies to their other projects.

Let’s use the figure from New Jersey as a template and assume that, because capacity is delivered as it comes online rather than when the entire project is completed, the actual cash required for buildout is about 12% lower than the stated cost.

Using my $10.4B capex number, Nebius would actually need around $9.15B in cash. They already have other capacity online or coming online that has been paid for, so it falls outside these capex calculations. That existing capacity is generating core adjusted EBITDA profitability, but expenses are inflated by costs related to their subsidiary Avride, so overall they’re still posting losses.

I also assumed all the revenue from Microsoft could be used directly for capex, but there are additional expenses tied to expanding capacity. For the Microsoft deal specifically, being bare metal, it’s less significant, but for their own AI cloud offerings, payroll expenses are large. This means Nebius still falls short in my estimates.

I see two possibilities here:

My estimates are wrong, either because of calculation errors or because Nebius has access to better pricing thanks to its relationship with NVIDIA.

Nebius is short on cash.

I’d say the truth is probably somewhere in the middle.

Funding options

If Nebius needs more funding, here’s what I think could happen:

Sell part of Avride: This seems the most likely option. Management has repeatedly said they’re looking for an investor. The Uber deal still feels like it’s hanging around. There’s also the possibility of a Hyundai deal, now that Hyundai is losing Waymo and its Motional joint venture is lagging behind.

A 30–50% buyout of Avride, maybe even up to 60%, could bring Nebius a few badly needed billions. I think it would be a mistake to value Avride at less than $8B, which I already see as conservative. So a deal in the range of $3–5B seems reasonable.

They could also tap the equity or debt markets further, depending on how the stock price behaves.

Valuation

Keep reading with a 7-day free trial

Subscribe to Daniel Romero to keep reading this post and get 7 days of free access to the full post archives.