My Meeting With LPKF’s CEO: Key Insights

What LPKF’s CEO told me about glass substrates, and the stocks I’m watching now

In this report, I’ll share, with explanations, what LPKF's CEO told me in our meeting, and how I am looking at glass substrates from an investment perspective, including other stocks in the supply chain.

Introduction

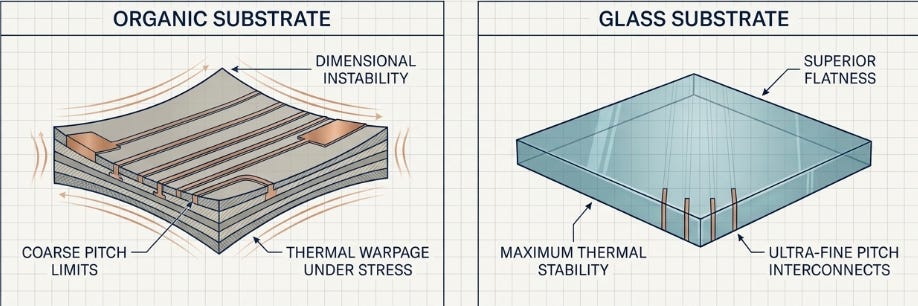

Traditional organic substrates are reaching limits in terms of flatness, warpage, thermal stability, and fine-pitch interconnects. Glass offers a much flatter and more dimensionally stable platform, which could make it a key material for the next generation of HPC packaging.

But glass is also difficult to process. To make it useful in advanced packaging, companies need to create thousands of extremely precise holes through the glass, called TGVs, or through-glass vias. These vias are then filled with copper so electrical signals can pass through the substrate.

This is where LPKF becomes relevant. The company’s core technology, LIDE, uses lasers and chemical etching to create these TGVs with very high precision. That is why LPKF has become one of the most discussed small-cap names in the glass substrate supply chain.

For my full deep dive on LPKF, including the company’s technology, valuation, and investment thesis, you can read my previous article here:

Semiconductor Bottleneck Microcap Stock

Over the last few months, I’ve been researching several companies in the semiconductor supply chain, specifically focused on those exposed to present and, more interestingly, future bottlenecks.

Market Share

The CEO told me they have 80% market share in TGV, and that they see this coming down to 70%. That would still be very impressive.

I continued by asking how the company would finance all that machine manufacturing if they achieved that market share.

I asked this because the balance sheet is not the most resilient.

Funding Expansion

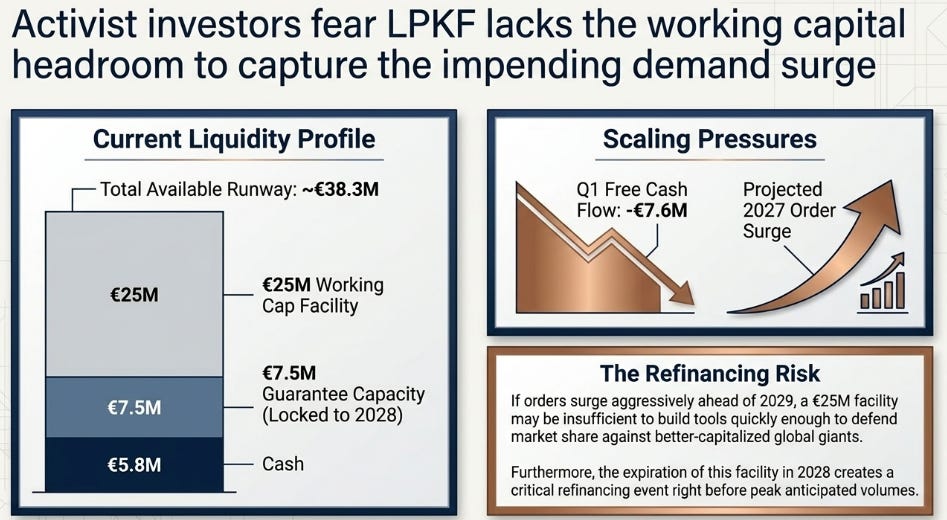

Q1 free cash flow was -€7.6M, they had €5.8M of cash, inventory was already rising ahead of deliveries, and the syndicated loan carries a €25M working capital facility, which exists precisely because a tool ramp consumes working capital.

This is why investor activists pushed for a raise. They think €25M of working capital headroom is not enough to build tools quickly and grab share before SCHMID, TRUMPF, and the domestic players scale.

Fiedler’s answer is that LPKF can scale with little money, meaning the facility, the 1.4 book-to-bill, and North Star cost cuts can get them there without dilution.

The risk he is accepting is clear. If 2027 orders surge, the company could become working capital constrained, unable to build enough machines right when the window opens.

They told me they are capex light and that they would not have a problem scaling.

I responded by asking how machine manufacturing can be capex light, and whether they would use third party manufacturing. They told me they could, but that they do not plan to do so, and that most of the expenses are electricity.

While counterintuitive, it can make sense.

LPKF does not manufacture the expensive parts of the machine, it buys them. The laser source comes from a laser maker, the precision optics from an optics house, and the motion stages, control electronics, handling systems, and vacuum systems from their respective vendors.

The capital-heavy work of actually producing a femtosecond laser or precision optics sits with those suppliers. LPKF’s job is to integrate all of it into a finished NEXAR tool, layer on the LIDE process IP and software, align it, test it, and ship it.

So its own plant is basically assembly bays, a cleanroom, alignment and test rigs, and engineers, not a billion-dollar production line.

Beyond what they have in cash, LPKF has €25M of drawable working capital headroom and €7.5M of guarantee capacity, locked until the end of 2028. That gives the company flexibility, but it is still modest.

First, the facility is small if production orders scale quickly. Second, it expires before the potential 2029–2030 high-volume phase, creating a refinancing event right before the biggest expected revenue years.

I mentioned this to him, and he told me he has talked with banks about possible financing if demand exceeds their capacity.

I do not know if he was referring to this facility. He mentioned it in relation to extra capital, and I would assume that if they actually get a large backlog, there would be banks willing to provide order-backed loans.

The Bottleneck

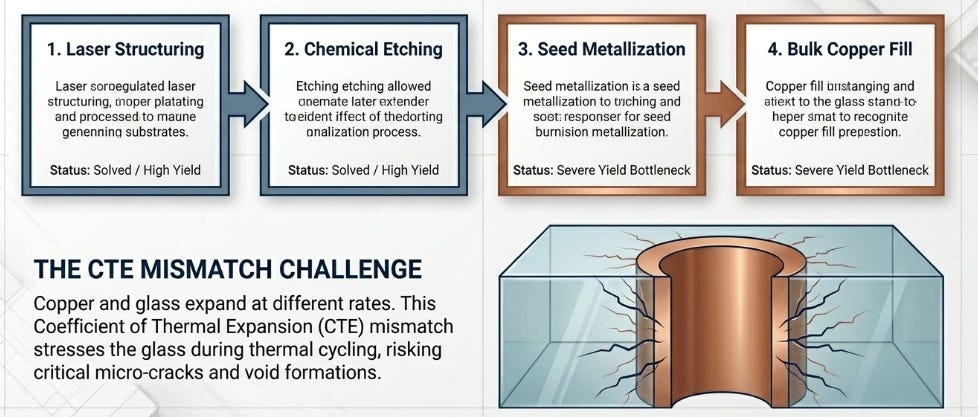

Fiedler told me TGV and LIDE are no longer bottlenecks for the glass substrate ramp. This process is qualified, and yields seem to be good enough, at least for low-volume production.

I asked him what the biggest problem to solve is in order to ramp glass substrates.

He told me that the biggest yield loss is not caused by TGV, but by metallization, which occurs when the holes etched through TGV are filled with copper.

The hardest parts are filling those holes with copper completely, with no voids, getting copper to adhere to glass, and most importantly, surviving thermal cycling.

Copper and glass expand at different rates. This is called CTE mismatch, or coefficient of thermal expansion. Every time the package heats and cools, that mismatch stresses the glass around each via and can crack it.

The leader in copper-to-glass adhesion is Atotech, part of MKS Instruments.

When I asked about it, he told me this is now fixed. In other words, if companies like SEMCO or Absolics are saying they will ramp through 2027 and 2028, it is because this is already working well enough.

But if glass substrates are still not at high enough yields, it is because of the copper fill step, not TGV.

Competition

Keep reading with a 7-day free trial

Subscribe to Daniel Romero to keep reading this post and get 7 days of free access to the full post archives.