Block: Deep Dive

Is the story really over?

Block is one of the most controversial companies in fintech. That is not surprising given its founder and CEO. Jack Dorsey has proven to be a great founder, with a creative mind capable of building successful products. However, his performance as CEO has been more debatable. Some strategic decisions, combined with the collapse of the 2021 bubble, pushed the stock down about 80% from its all-time high.

Even so, the company may be in its strongest operating shape yet. Revenue is still growing, Block has expanded with Afterpay, Tidal, Bitkey, and Proto, and margins are stronger than in prior years.

While retail sentiment remains broadly bearish, Wall Street has turned more constructive. Most analysts now rate the stock as a buy, and that trend has strengthened in recent months.

So the question is: should retail start looking at Block in a different light?

The Rise and Fall

Block, previously known as Square, was one of the hottest stocks in 2021, reaching 273 dollars versus about 54 dollars today. Square was extremely popular among retail investors and became a top pick across social media. It was not only retail enthusiasm either, analysts had an average price target near 260 dollars in July 2021.

A few examples:

Deutsche Bank had a 330 dollar target

Mizuho Financial Group set a 380 dollar target

Dan Dolev said buying Square was like buying JP Morgan in 1871

Square was framed as the future of fintech, praised for growth, modern execution, and Jack Dorsey’s long-term vision. But it was also part of a broader bubble, like many stocks at the time. The difference is that while other fintech names have recovered a meaningful part of their losses, Block has remained under pressure.

The Tidal Misstep

Block reached its peak market capitalization in August 2021 at around 127 billion dollars, shortly after the Tidal acquisition. The company issued new shares to acquire an 88% stake for 297 million dollars in a relatively niche music streaming platform.

The deal immediately raised questions. Why was a fintech company acquiring a music service?

Skepticism increased because one of Tidal’s primary owners was Jay-Z, a close associate of Jack Dorsey. After the acquisition, Jay-Z joined Block’s board and still holds that position.

The move also created internal friction. According to employee reports, management issued strict warnings about mentioning Shawn Corey Carter in internal communications.

Criticism grew quickly. Many investors saw the deal as diworsification, not strategic diversification.

Some argued Tidal could eventually integrate with Square or Cash App in meaningful ways, but that thesis did not materialize. Tidal lost support on key distribution platforms such as Samsung TV, Roku, and Plex. Through 2023 and 2024, the business went through heavy layoffs, and Block later acknowledged it was reducing investment in the segment.

Afterpay and Dilution

In December 2021, Block acquired Afterpay in an all-stock transaction, issuing more than 113 million shares and valuing the deal at 13.9 billion dollars. That implied dilution of roughly 20% to complete the acquisition.

Many investors viewed this as another case of overpaying, and the concern was understandable. By closing, Afterpay’s implied valuation was around 29 billion dollars, close to Block’s current market value near 33 billion dollars.

Similar to other peak-cycle acquisitions in that period, the market argued that Block leaned too far into qualitative upside while underweighting valuation discipline and cycle risk. The outcome was expensive deals that weighed on the stock for years.

The Fundamentals Broke Down

And that was not the only issue.

Block’s sales grew 85% in 2021, a huge figure that fueled market hype. But one year later, that growth turned negative. Profitability weakened sharply. Revenue momentum slowed while operating expenses rose about 50%, largely due to an oversized cost structure. The business turned unprofitable.

So the setup was brutal: a 2021 bubble, the controversial Tidal acquisition, heavy Afterpay dilution, and a sudden operating slowdown. That combination drove a major rerating, and Block fell more than 60% in 2022.

Cleaning Up the Mess

The story started to shift in 2023 and 2024.

There have been layoffs. The TBD project was shut down. Investment in Tidal was reduced. And the company is finally focused on its core priorities:

Cash App

Square

Integration of buy now, pay later across products

Expansion of its Bitcoin ecosystem through Bitkey and Proto

You could frame this as a company resetting after a period of strategic drift. It is cutting distractions and returning to its strongest assets.

That shift is driving one central question for investors:

Is this now a buying opportunity?

Let’s explore it.

Cash App

Cash App is a mobile financial platform that allows users to send, receive, spend, invest, and borrow money through a clean, intuitive interface. It competes directly with Venmo, Zelle, and Apple Pay, and to some extent with Robinhood, Chime, and Coinbase.

It is currently the most used financial app in the United States.

It is extremely popular among younger users and is evolving into a true all-in-one financial app. By stacking multiple services into one product, it has expanded from a simple payments tool into a banking interface, investment platform, and crypto wallet in one place.

To start, Cash App has effectively become a bank-like platform.

It is the fourth-largest debit card issuer in the United States and the fastest-growing.

Historically, like many fintech platforms, Cash App had a major limitation in lending: it depended on external banking partners. That is no longer the case, and it is a meaningful shift.

Block now operates its own bank, Square Financial Services. It already provides business loans within the Square ecosystem. Until recently, however, Cash App did not have approval for direct consumer lending through that entity.

That has changed. With the required FDIC approval in place, Square Financial Services can now originate loans directly to Cash App users.

This is a major development. Block is the only major fintech with a wholly owned, FDIC-approved bank, and that unlocks important advantages:

Tighter vertical integration across the financial stack

Faster settlement, supporting better cash flow for users and merchants

Greater control over risk, compliance, and lending margins

Which can translate into:

Margin expansion

Faster loan growth

Deeper monetization of Cash App’s 57 million plus users

The timing is also strong. Cash App Borrow originations are expected to reach about 9 billion dollars in 2024, up roughly 150% year over year. With Square Financial Services now Ifunding these loans internally, unit economics can improve materially. As volume and lending margins scale together, earnings leverage should increase.

It is not only Cash App. Square Capital, the lending arm of Square, is already originating around 5.7 billion dollars in loans, growing about 19% year over year.

Owning an internal, FDIC-approved bank gives Block a durable competitive edge through stronger take rates, interest income, and operating margins.

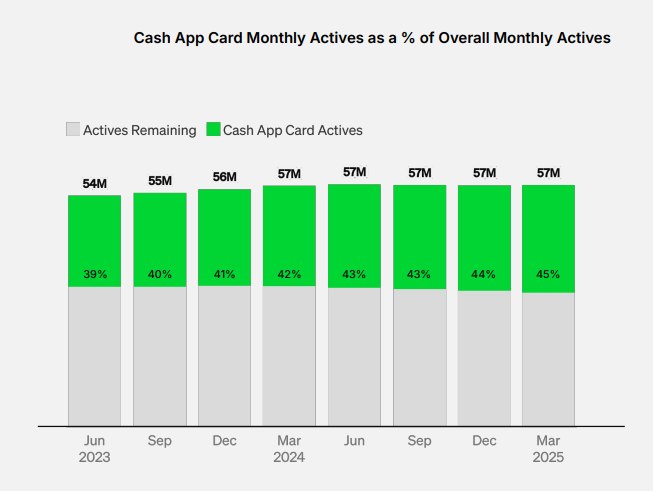

On revenue dynamics, growth in new active users has flattened near 0%, which is understandable at this scale. Cash App is currently United States-focused and already serves around 57 million monthly transacting actives, roughly one-fifth of the adult population.

Cash App grew gross profit by 10% last quarter, reaching an annualized run rate of about 5.5 billion dollars. On that basis alone, Block is trading at roughly 6.4x Cash App gross profit.

Cash App and Afterpay

Cash App is now integrating Afterpay directly into its platform.

Afterpay United States is being rebranded as Cash App Afterpay, allowing users to pay with their Cash App Card or directly inside the app through buy now, pay later features.

This is a major distribution upgrade for Afterpay, which now gets direct access to Cash App’s 57 million active users. It is also a strategic win for Cash App, given its strong position with Gen Z, a cohort that is more comfortable with BNPL than traditional credit cards.

The behavioral shift is clear.

A 2025 J.D. Power study found that 42% of Gen Y and Gen Z consumers used BNPL, versus 21% of older consumers. During the 2024 holiday season, Gen Z users chose BNPL over credit cards for the first time in that study’s history.

These users are actively seeking more flexible repayment structures, and BNPL is becoming a preferred tool.

So the setup now is:

The largest financial app for Gen Z

Integrated with Afterpay

Lending capacity supported by Block’s FDIC-approved bank

Block’s long-term ecosystem strategy is becoming more visible.

And Afterpay is a meaningful asset. It is one of the largest BNPL platforms globally. Originating in Australia, it remains strong in its home market and is now one of the largest BNPL providers worldwide, alongside leaders like Klarna and PayPal.

While Afterpay’s take rate is lower than Affirm’s, its gross profit is still relatively close:

Afterpay: 970 million dollars

Affirm: 1.25 billion dollars

Affirm is growing faster, but Afterpay is still delivering solid performance, with 22% year-over-year GMV growth.

What stands out is this:

Afterpay is still a smaller piece of Block’s overall mix compared with Cash App at about 5.24 billion dollars in gross profit and Square at about 3.6 billion dollars. Even so, it remains competitive with Affirm on absolute economics, while Affirm trades at roughly half of Block’s market capitalization.

That points to one of two conclusions:

Either Affirm is overvalued, or Block is undervalued.

Possibly both.

Square

")

Just as Cash App serves consumers, Square serves businesses. It is an integrated ecosystem designed to help merchants run operations across physical and digital channels.

Square is a merchant services and point-of-sale platform that helps small and medium-sized businesses accept payments, manage operations, and access financing. It started as a simple card reader connected to smartphones, then evolved into a broader commerce and financial platform.

It competes with PayPal, Shopify POS, Toast, Clover, and legacy providers such as NCR.

Today, Square offers services across nearly every core business function:

Point-of-sale and payment hardware

Software solutions

Online and e-commerce tools

Financial services

Invoicing, loyalty, and customer relationship tools

Developer APIs

Square revenue is growing around 7.2%, while gross profit rose 9% to about 898 million dollars.

Although the lower growth rate is a concern, context matters. The United States economy showed tariff-related softness, and consumer spending grew only 1.6%. That helps explain why a business so exposed to consumer activity is seeing slower momentum.

Over the long term, as Square continues expanding its product suite and lending capabilities, growth can remain steady as more merchants migrate to a modern, integrated ecosystem with very high customer satisfaction.

Bitkey

Bitkey is a self-custody Bitcoin wallet developed by Block.

It is one of Jack Dorsey’s most ambitious initiatives, designed to help people secure and control their Bitcoin without depending on centralized exchanges or custodians.

Bitkey is not only an app, it is a full system that combines:

A mobile app

A hardware device

Cloud backup infrastructure

The objective is to make self-custody simpler and safer for everyday users.

Unlike many wallets, Bitkey uses a three-key multisignature design to balance security and recoverability. It is built to:

Lower the technical barrier to self-custody

Help users in emerging markets hold Bitcoin more safely

Offer a middle ground between usability and sovereignty

Bitkey fits into Block’s broader Bitcoin strategy, alongside initiatives such as mining and Lightning-related infrastructure through Spiral.

Adoption is still early, but the backdrop is shifting. With higher Bitcoin adoption, broader use cases, and increasing demand for secure storage, Bitkey could become another meaningful layer in the broader Block ecosystem.

Proto

Proto is one of Block’s newer ventures, focused on building Bitcoin mining ASICs and full rack systems, with the objective of creating one of the most competitive miners in the market. It fits directly into Block’s broader Bitcoin ecosystem strategy.

This could become a meaningful growth driver.

The Bitcoin mining hardware market is expected to exceed 25 billion dollars by 2030. Today, much of that hardware is imported from China. Block is aiming to build a United States-based alternative with stronger performance and reliability.

To execute on that plan, Proto is:

Developing 3-nanometer mining chips manufactured by TSMC

Collaborating with Core Scientific on mining rig design

To underscore commercial traction, Core Scientific has already prepaid about 21.3 million dollars for these ASIC systems, with delivery expected by the third quarter of 2025.

The Bitcoin Bet

Block is one of the most Bitcoin-bullish public companies, and that is reflected not only in its products but also in its balance sheet. It currently holds the tenth-largest corporate Bitcoin treasury globally, with 8,594 bitcoins, valued at roughly 914 million dollars.

To continue building that position, Block announced in the second quarter of last year that it would allocate 10% of monthly gross profit from Bitcoin products to buy more Bitcoin. This is clearly a controversial decision and, in my view, it has added to Wall Street’s skepticism toward the company.

So investing in Block is not only a fintech thesis. It also includes direct exposure to an asset class that many investors still view cautiously.

Tidal and AI Bets

For now, Tidal contributes little to Block’s valuation and remains a wildcard. But if Block integrates Tidal more deeply into its ecosystem and applies AI effectively, it could become an unexpected catalyst.

As Jack Dorsey has suggested, Tidal could evolve into a platform similar to a business operating system for musicians, helping manage royalties, payments, fees, expenses, and operational tools that save time and improve economics for artists.

To differentiate Tidal from traditional streaming platforms, Block can leverage its product talent and AI investment strategy. The company is actively investing in AI to improve usability and performance, a key requirement as younger users increasingly expect seamless digital experiences.

To support that push, Block has invested heavily in infrastructure and became the first company in North America to deploy NVIDIA GB200 systems.

Block is already integrating AI into the Square platform. It recently launched Square AI, designed to give sellers smarter tools that automate operations and save time, including:

Menu generation for restaurants

AI image editing for e-commerce

Email copywriting tools

Website building tools

AI-assisted business communications

These tools are expected to expand over time.

And if Block is innovating aggressively inside Square, there is a fair question: why not apply the same product intensity to Tidal?

Potential features such as AI-assisted music creation, smarter playlist systems, and advanced editing workflows could reposition Tidal from a weak asset into a differentiated platform.

Of course, that remains speculative. Block has historically moved slowly in some product areas. Still, the company now appears to be in a more execution-focused phase.

On May 14, Block released the largest product update in its history, launching more than 100 new products and features.

This followed a disappointing earnings release, after which shares fell more than 10%. The product launch does not fully change valuation on its own, but it does signal renewed urgency and strategic intent.

Among the announcements, Square Handheld stood out, a portable point-of-sale device that helps sellers manage payments and back-of-house tasks such as table service and inventory workflows.

Square Handheld offers one of the strongest feature sets compared with similar devices from competitors:

This renewed push in innovation and product development is exactly what Block needs in a highly competitive market where staying at the frontier matters. Even now, there are few alternatives that match its overall merchant product quality. Over the long term, Block’s emphasis on product depth and execution can remain a meaningful advantage.

Financials

Block has moved from a pure hypergrowth phase into a transition phase, learning to operate as a scaled platform company.

It can no longer run like an early-stage startup. It needs tight product integration across a unified ecosystem. In my view, the numbers reflect that shift clearly: slower top-line growth, improving profitability, and a setup for a potential new growth cycle.

Key year-over-year metrics from the last quarter:

Revenue excluding Bitcoin: +9%

Gross profit: +7.6%

Adjusted EBITDA: +15%

Adjusted operating income: +28%

In summary, growth is steady and margin expansion remains strong.

Full-year guidance is not spectacular, but the direction is positive.

Full-year 2025 guidance:

Gross profit growth: 12% year over year

Rule of 40: 31%

So overall, the numbers are solid, even if not yet exciting. More execution will be needed to fully rebuild investor confidence. But if this is truly a transition phase, and you focus on the long-term potential of the ecosystems Block is building, a 36 billion dollar valuation does not look stretched.

For that valuation, you are buying:

The most popular financial app in the United States

A leading BNPL platform across Australia, the United Kingdom, Canada, New Zealand, and the United States

An all-in-one ecosystem for businesses spanning financial and commerce needs

A wholly owned, FDIC-approved bank

Plus Proto, Tidal, Bitkey, and an internal AI team that could become a real differentiator versus other fintech platforms

Looking Forward

The most compelling part of Block is its vision: building a fully integrated digital ecosystem across finance and commerce. The strategy is to connect its diverse, high-quality products into one seamless experience, so businesses and consumers have fewer reasons to leave. That integration is now starting to become visible.

Cash App and Square already hold strong positions in their markets. Both score well on customer satisfaction and continue to ship features users value. That product momentum slowed for a period, but Block is accelerating development again, especially within Square, which helps restore confidence in management’s long-term strategy.

The end goal is an ecosystem of ecosystems, linking the business hub (Square) with the consumer hub (Cash App), and vertically integrating lending through Afterpay and Square Financial Services.

Beyond that, Block wants Bitcoin to be a core layer of this platform. Management has discussed enabling Bitcoin payments, potentially through the Lightning Network for faster, lower-cost transactions. The strategy also extends to infrastructure, including mining chips and systems through Proto, plus self-custody through Bitkey.

Tying this together is an in-house AI strategy, supported by NVIDIA GB200 systems, with the objective of improving usability, automation, and performance across the full product stack.

Market skepticism is understandable. When a company pursues many initiatives at once, execution risk rises. But the opportunity is large, and if Block successfully integrates this vision, today’s valuation could look like an early entry point into a misunderstood platform company.

Block looks like a value trap. It’s caught in a squeeze from both sides—Affirm is outpacing it in BNPL (Affirm’s GMV jumped 34.7% YoY to $10.1 billion in Q2 FY 2025), while its crypto push via Cash App runs headlong into Coinbase’s scale and breadth (Coinbase serves over 108 million customers). On top of that, Block’s sprawling ambitions—from Square merchant services to Tidal and Spiral—raise the bar for near-perfect execution, leaving little room for any one segment to stumble.

Good analysis you made very compelling points. I did a similar one on Shift4 if you want to check it out.